Machine Learning in Banking IT

AI in Banking IT – Pt. 2

Artificial intelligence (AI) is a rapidly evolving field with a cornucopia of usages and benefits everywhere you look. Banking IT is no exception. But what does AI entail? What kind of processes does it build on? What makes it so versatile? This series on AI in banking IT will give a glimpse into the key fields of AI and where and how they are used in banking IT operation. This instalment discusses Machine Learning.

Machine Learning

As we have already established in the first part of this series on AI, Machine Learning (ML) is a subset of Artificial Intelligence. In the case of ML, we ask machines to do things over and again not, until they recognise patterns and differences that help make sense of the data in front of it.

These machines learn from experience and improve the parameters of their code. One must remember, however, that the machine still cannot think, so their answers and the changes in parameters are educated guesses. These guesses, predictions, and improvements, however, are only as good as the questions we asked them the datasets used in the process.

Machine Learning Types

The methods ML uses to arrive at its conclusions are many, but taking a simplistic approach they can be categorized into three (plus one) major learning types. These depend on the type of input, output, layers and processes involved, i.e. the algorithms used.

Supervised Learning

STEP 1. The computer is fed with training data where the input and the expected output are all labelled. The computer analyses the training data for patterns and learns its logic, i.e. function.

STEP 2. The computer uses the function (approved by human experts) for its decision and predictions based on new input data.

Unsupervised Learning

The computer has to make sense of unlabelled data, discover its internal structure without predefined output categories.

STEP 1. The algorithm searches for rules and patterns

STEP 2. It groups data points according these patterns/models, so users can understand data better.

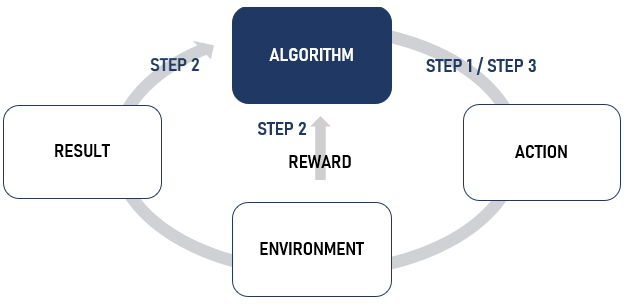

Reinforcement Learning

This type of learning is a trial and error type of learning.

STEP 1. The computer observes the state of the environment (input) and its target. It decides on a course of action.

STEP 2. As a result of this action, it receives a reward (feedback) from the environment. It stores the action-result pairs.

STEP 3. Its goal is to maximize the reward, so it tries to optimize its decisions to achieve this.

Learning Types Summary

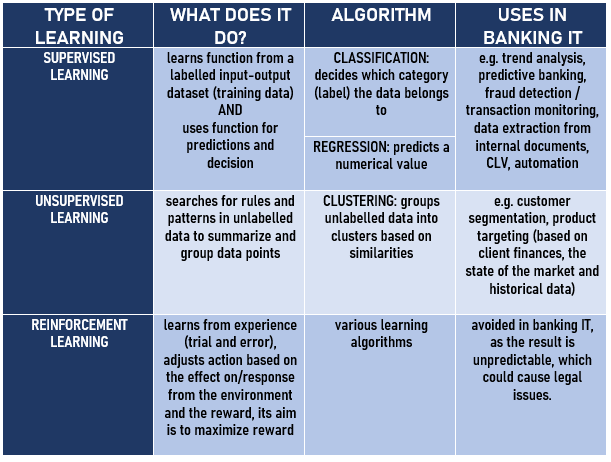

Below, you’ll find a table summarizing the different types of ML, their most common algorithms (classification, regression, and clustering), as well as their uses in banking IT. Of course, more often than not they are applied in combination – for instance, customer lifetime value prediction (CLV), listed under supervised learning would be impossible without prior customer segmentation (performed by a dedicated unsupervised learning algorithm).

ROI on Machine Learning

The beneficial effect of ML is indeed quite extensive in banking IT which also shows in the relevant ROI. Take, for instance the fact that by the automation of certain time and resource-intensive tasks, such as the extraction of data from documents (supervised learning), ML can not only save banks immense costs, but also prevent manual errors happening in the same process.

A great example was the introduction of the software called COIN (Contract Intelligence) at JP Morgan, which reportedly saved 360,000 hours of lawyer’s time in document reviews – and performed the same task in seconds, with more accurate results.

But there is more to ML than parsing documents. Here are some key areas in which your financial institution can also profit from implementing ML solutions:

- fraud detection (real-time and statistical monitoring/analysis),

- regulatory compliance (augmenting and scaling the skills of the compliance offers),

- operation (automation, error prevention, trend analysis),

- customer experience (improved insight and faster decision making, chatbots), and

- customer engagement (customized products and services, advisory features).

What’s next…

The next blogpost in this series will focus on Deep Learning in Banking IT, specifically on Generative Adversarial Networks (GAN) techniques.